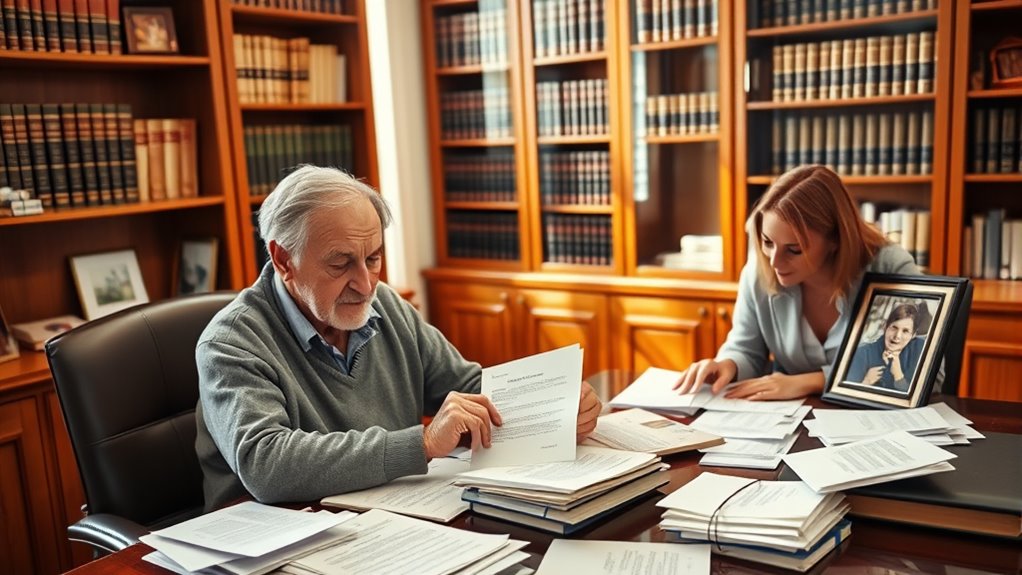

After your parent’s passing, start by gathering important legal and financial documents like wills, deeds, and insurance policies. Notify relevant institutions and consider how inheritance taxes may affect your estate. Organize assets carefully, decide whether to sell or keep property, and update any estate plans as needed. Clear communication with family members helps prevent conflicts. Continuing will guide you through key steps to manage the estate efficiently and honor your parent’s wishes.

Key Takeaways

- Collect and organize all relevant legal and financial documents, including wills, property deeds, and bank statements.

- Notify financial institutions, service providers, and family members about the parent’s passing.

- Review and update estate plans, considering asset distribution, tax implications, and future needs.

- Consult estate planning professionals to navigate legal requirements and minimize inheritance taxes.

- Communicate openly with family members to prevent conflicts and ensure smooth estate settlement.

Managing estate matters can be complex and emotionally challenging, but taking a proactive approach helps guarantee your wishes are honored and your loved ones are supported. When navigating the aftermath of a parent’s passing, one of your primary concerns will likely be understanding and managing inheritance taxes. These taxes can significantly impact the estate’s value, so it’s crucial to be aware of your jurisdiction’s laws and thresholds. Some states or countries impose inheritance taxes based on your relationship to the deceased or the amount inherited, which can reduce the overall inheritance received by your family. To minimize surprises, it’s wise to consult with a financial advisor or estate planning attorney early in the process. They can help you explore strategies to reduce inheritance tax liabilities, such as establishing trusts or making strategic gifts during your parent’s lifetime.

Understanding inheritance taxes and consulting professionals early can help protect your family’s assets and honor your loved one’s wishes.

Estate planning plays a vital role in ensuring a smooth transition after a loved one’s death. If your parent had a comprehensive estate plan, it likely includes a will, trusts, or other legal instruments that specify how assets should be distributed. Reviewing these documents carefully allows you to understand their intentions and identify any potential issues. If no estate plan exists, you may need to initiate the probate process, which can be time-consuming and emotionally draining. In either case, working with professionals can help you navigate legal requirements efficiently. They can also assist in valuing estate assets, resolving disputes, and ensuring all debts and taxes are paid before distribution.

Another essential aspect of managing estate matters involves organizing financial and legal documents. Gather all relevant records, such as wills, bank statements, property deeds, and insurance policies. This organization not only simplifies the process but also ensures nothing gets overlooked. Communicate with financial institutions and service providers to notify them of the death and to handle accounts properly. If the estate includes real estate, consider whether to sell or retain properties, keeping in mind potential tax implications and future needs. Throughout this process, prioritize transparency with other family members, maintaining open communication to prevent conflicts and misunderstandings. Additionally, understanding risk assessment for merchant services can be helpful if managing estate assets involves digital transactions or online estate management platforms.

Finally, remember that managing estate matters is an ongoing process. Regularly review the estate plan and update it as circumstances change—such as new assets, debts, or family dynamics. By staying organized and informed, you can handle inheritance taxes efficiently and ensure your parent’s wishes are fulfilled, providing peace of mind for yourself and your loved ones.

Frequently Asked Questions

How Do I Locate All of My Parent’s Hidden Assets?

To locate your parent’s hidden assets, start by reviewing financial statements, tax returns, and bank records for unusual transactions. Check safe deposit boxes, online accounts, and mail for overlooked items. Talk to family members or trusted advisors who may have insights. Consider hiring a professional, like a forensic accountant, to assist with asset discovery. They can uncover hidden assets and guarantee you get a complete picture of your parent’s estate.

What Are the Tax Implications of Inheriting Certain Assets?

Think inheriting assets is just a windfall? Think again! The tax implications can be sneaky, affecting your estate planning and tax strategies. You might owe estate taxes or capital gains if you sell certain assets. Depending on the type of inheritance, you could face income tax or estate tax, so consult a professional. Staying aware helps you maximize benefits and avoid surprises down the road.

How Can I Prevent Family Disputes Over the Estate?

You can prevent family disputes by fostering open family communication and creating a thorough estate plan. Make sure everyone understands your wishes clearly and involve family members in the planning process. Document your decisions carefully, including wills and trusts, to avoid confusion. Regularly review and update your estate plan to reflect any changes. Clear, transparent communication combined with solid estate planning helps minimize misunderstandings and keeps family harmony intact.

What Steps Should I Take if a Beneficiary Contests the Will?

Think of will contesting like a tug-of-war; it can pull families apart. When a beneficiary disagrees with the will, you should consult an attorney promptly to review the legal grounds for contesting. Gather all relevant documents, like the will and any evidence of undue influence. Communicate openly with family members, but avoid making promises. Addressing beneficiary disagreements early can help prevent prolonged disputes and preserve relationships.

How Long Does the Estate Settlement Process Typically Take?

The estate settlement process usually takes several months to over a year, depending on the probate process and estate valuation complexity. You’ll need to gather all assets, pay debts, and settle taxes, which can extend the timeline. As you navigate these steps, expect delays if disputes or legal challenges arise. Staying organized and working closely with an attorney helps guarantee you move through the estate settlement efficiently.

Conclusion

Handling estate matters after a parent’s passing can feel overwhelming, but remember, you’re like a skilled captain steering through uncertain waters. Stay organized, seek professional guidance when needed, and communicate openly with family members. By taking things step by step, you’ll navigate this challenging time more smoothly. Trust yourself to manage these responsibilities with compassion and clarity—just as a steady hand keeps a ship on course amid turbulent seas.